[ad_1]

Darius Dale is the Founder and CEO of 42 Macro, an funding analysis agency that goals to disrupt the monetary providers business by democratizing institutional-grade macro danger administration processes.

Key Takeaways

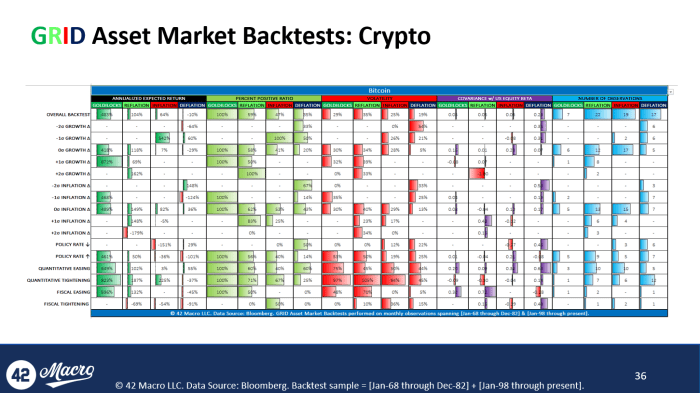

The distribution of possible financial outcomes — and by extension, monetary market outcomes — is as flat and broad because it has been in recent times. 42 Macro’s base-case state of affairs of deflation requires an anticipated return of -10% annualized for bitcoin. Our bull case state of affairs of deflation plus coverage fee decreases requires an anticipated return of +29% annualized for bitcoin. Our bear case deflation plus quantitative tightening requires an anticipated return of -37% annualized for bitcoin. Critically, all three situations are equally possible over the subsequent three to 6 months. If we sounded extremely satisfied issuing promote warnings at each decrease excessive in bitcoin’s value from early-December via July, we should always sound equally unconvinced at this time.

(Chart by 42 Macro)

(Chart by 42 Macro)

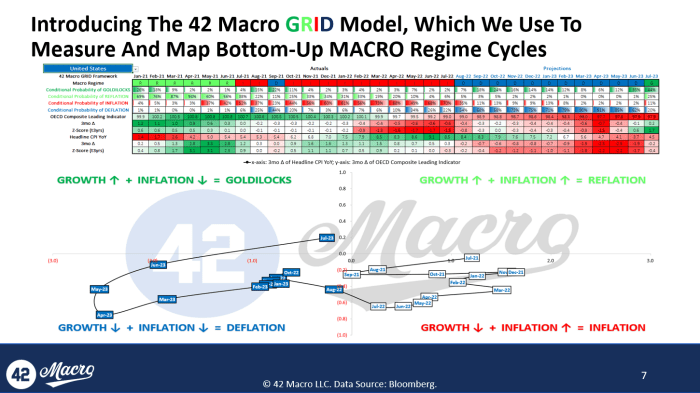

The Base Case

U.S. and international development proceed to gradual, albeit at a extra modest tempo than in current quarters. The Fed and different central banks proceed to procyclically tighten financial coverage via 12 months finish: soft-ish touchdown.

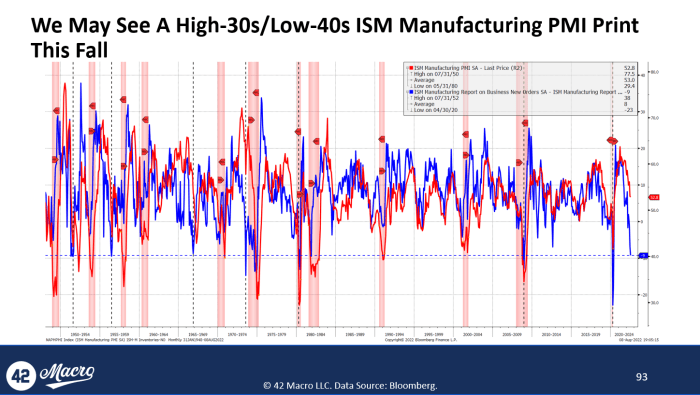

Bayesian highlight: The slowdown within the headline ISM Manufacturing to the bottom stage since June 2020 was an afterthought relative to the decline within the “new orders much less inventories” unfold falling to -9. That is the bottom stage since December 2008. There have solely been eight such situations the place the unfold troughed at present or worse ranges. The median trough ISM Manufacturing studying in such situations is 38.6, which is usually reached one month in a while a median foundation. The median trough ISM Manufacturing studying when the unfold troughs +/- 1 level from its present stage of -9 is 42.5, which is usually reached three months in a while a median foundation (n=4). All informed, it might be smart for traders to emphasize check their portfolio holdings for, at greatest, a low-40s ISM Manufacturing statistic this fall.

(Chart by 42 Macro)

(Chart by 42 Macro)

The Bull Case

U.S. inflation momentum continues to say no sharply, seemingly inflicting the Fed to pause after a remaining fee hike in September. The development in actual incomes pulls ahead the constructive inflection in development: smooth touchdown.

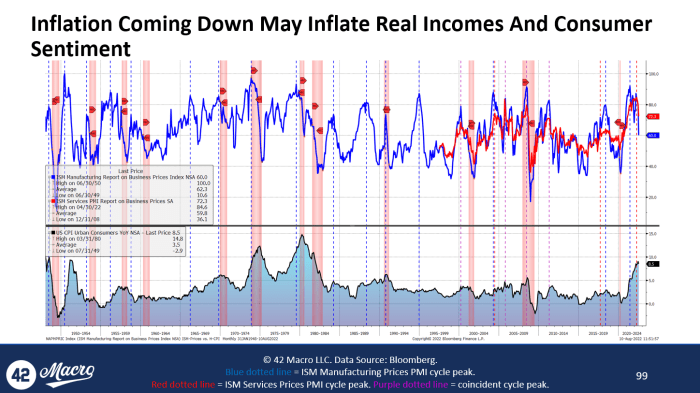

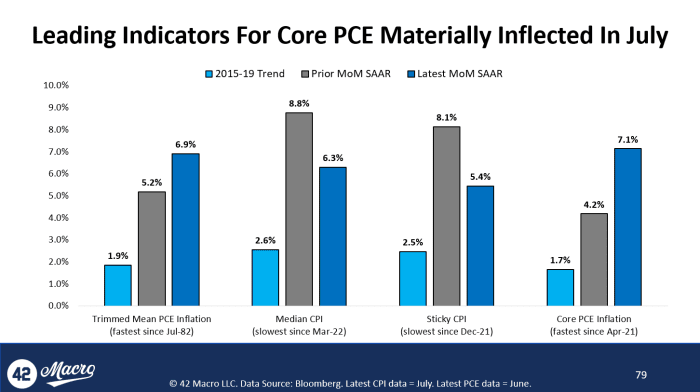

Bayesian highlight: The July client value index (CPI) launch represented the river card in a trifecta of knowledge factors: July ISM Providers PMI, July Jobs Report, July CPI, that each one lend credence to the soft-landing view. Whereas the draw back surprises on each headline CPI (0.0% month-over month versus 0.2% estimate) and core CPI (0.3% month-over-month versus 0.5% estimate) have been to be celebrated, the brunt of the excellent news got here by way of the sharp slowdowns in median CPI (-250 foundation factors to six.3% month-over-month annualized) and sticky CPI (-270 foundation factors to five.4% month-over-month annualized) as a result of these indicators monitor core private consumption expenditures (PCE) — the Fed’s most popular inflation gauge — higher than most different CPI time collection. If the deceleration in these main indicators continues on the identical tempo and if historic correlations persist, we could possibly be month-over-month annualized charges of core PCE of roughly 2% within the August or September information. These are clearly two very massive ifs, particularly contemplating we’re devoid of historic examples of this sort of non-recessionary inflation dynamism to adequately prepare a mannequin on. At any fee, the likelihood the Fed could possibly be heading into its November 2 assembly with “clear and confirming proof” that inflation is more likely to pattern again in the direction of its 2% goal in an affordable timeframe is surprising to sort, however sort it we should, contemplating August PCE is launched on Sept. 30 and September PCE is launched on Oct. 23.

(Chart by 42 Macro)

The Bear Case

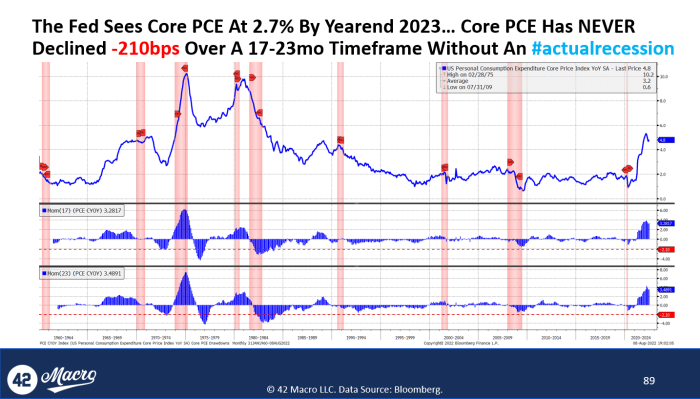

The nascent deceleration in inflation momentum stalls out at ranges inconsistent with the Fed’s value stability mandate, inflicting the Fed to tighten nicely into 2023: onerous touchdown.

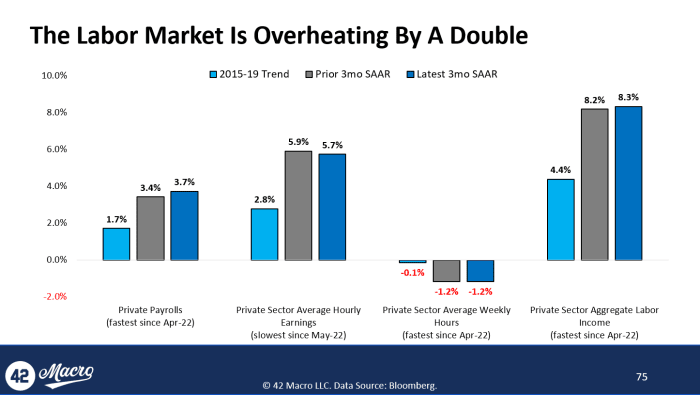

Bayesian highlight: The labor market is overheating by a double, relative to pre-COVID developments. The hotly debated 528k month-over-month “headline nonfarm payrolls” determine for July clearly stole the present from a market response perspective. The reacceleration within the three-month annualized development charges for headline (+40 foundation factors to a three-month excessive of three.5%) and personal payrolls (+30 foundation factors to a three-month excessive of three.7%) is suggestive of a home labor economic system that’s not responding to the coverage tightening now we have gathered to date. With the three-month annualized development fee of personal sector common hourly earnings slowing modestly (-20 foundation factors to a two-month low of 5.7%) alongside unchanged personal sector common weekly hours development of -1.2%, it’s clear the +10 foundation factors uptick in combination personal sector month-to-month earnings — to a three-month excessive of 8.3% — was largely pushed by extra staff discovering work.

(Chart by 42 Macro)

(Chart by 42 Macro)

It is a visitor publish by Darius Dale. Opinions expressed are solely their very own and don’t essentially replicate these of BTC Inc. or Bitcoin Journal.

[ad_2]

Source link

Be the first to comment